Housing And Civil Enforcement Cases Documents

IN THE UNITED STATES DISTRICT COURT FOR THE

NORTHERN DISTRICT OF ILLINOIS

UNITED STATES OF AMERICA,

Plaintiff,

v.

FIRST AMERICAN BANK,

Defendant.

COMPLAINT

The United States of America alleges:

1. This action is brought by the United States to enforce the provisions of Title VIII of the Civil Rights Act of 1968, the Fair Housing Act, as amended by the Fair Housing Amendments Act of 1988, 42 U.S.C. §§3601-3619, and the Equal Credit Opportunity Act, 15 U.S.C. §§1691-1691f.

2. This Court has jurisdiction of this action pursuant to 28 U.S.C. §1345, 42 U.S.C. §3614, and 15 U.S.C. §1691(h). Venue is appropriate pursuant to 28 U.S.C. §1391.

3. Defendant First American Bank (hereinafter "First American" or "Bank") is an Illinois state-chartered full service bank headquartered in Carpentersville, Illinois, and doing business primarily in the State of Illinois. The Bank is a subsidiary of First American Bank Corporation, a bank holding company incorporated in 1984 under the laws of the State of Delaware.

4. First American offers the traditional services of a financial depository institution, including the receipt of monetary deposits; the financing of residential housing, commercial, and consumer loans; and other types of credit transactions. As of March 31, 2004, First American Bank had total assets of $1.9 billion and over $1.7 billion in deposits. First American was subject to the regulatory authority of the Federal Reserve Board (hereinafter "the Board") until November 24, 2003; since that time, the Federal Deposit Insurance Corporation has been its regulator.

5. The Bank is subject to the federal laws governing fair lending including the Fair Housing Act, the Equal Credit Opportunity Act, and the Community Reinvestment Act ("CRA"), 12 U.S.C. §§2901-2906, and the regulations promulgated under each of those statutes. The Fair Housing Act and the Equal Credit Opportunity Act prohibit financial institutions from discriminating on the basis of, inter alia, race, color, or national origin in their lending practices.

6. Beginning in January 2001, the Federal Reserve Board conducted an examination of the lending practices of First American Bank to evaluate its compliance with the Fair Housing Act, the Equal Credit Opportunity Act, and the Community Reinvestment Act. Based on information gathered in its examination, the Board determined that it had reason to believe that First American was engaged in a pattern or practice of discrimination on the bases of race and national origin by redlining majority minority census tracts - defined as those with non-white populations of 50% or greater - in the Chicago and Kankakee, Illinois, metropolitan areas. The Board determined that the Bank was engaged in practices which prevented or discouraged the residents of those census tracts from obtaining equal access to residential, consumer, and small business credit because of the race, color, or national origin of the majority of the tracts' residents. The Board also lowered First American's CRA rating to "Substantial Noncompliance", the lowest possible. Of the 312 lending institutions the Board rated for CRA compliance between July 1, 2001, and June 30, 2002, First American was the only lender to receive that rating; the Board rated 40 lenders as "Outstanding", 270 "Satisfactory", and 1 "Needs to Improve".

7. Pursuant to 15 U.S.C. §1691e(g), the Board referred the matter to the Attorney General on May 14, 2002, for appropriate enforcement action, following the Board's determination as described in Paragraph 6.

8. First American Bank originated in the 1980s from the consolidation of eight smaller Chicago and Kankakee metropolitan area banks. By 1995, those banks had been further consolidated into three banks - First American Bank, Carpentersville; First American Bank, Kankakee; and First American Bank, Joliet. In September 1999, First American Bank Corporation consolidated the charters of those three institutions into one charter, First American Bank, Carpentersville, Illinois. By January 2003, First American had grown to a network of thirty-four branch offices located throughout the Chicago/Kankakee region. Throughout this time period, the banks were all operated under the same management.

9. The Chicago Metropolitan Statistical Area (hereinafter "Chicago MSA"), as defined by the United States Census, includes nine counties - Cook (including the City of Chicago), DeKalb, DuPage, Grundy, Kane, Kendall, Lake, McHenry, and Will.

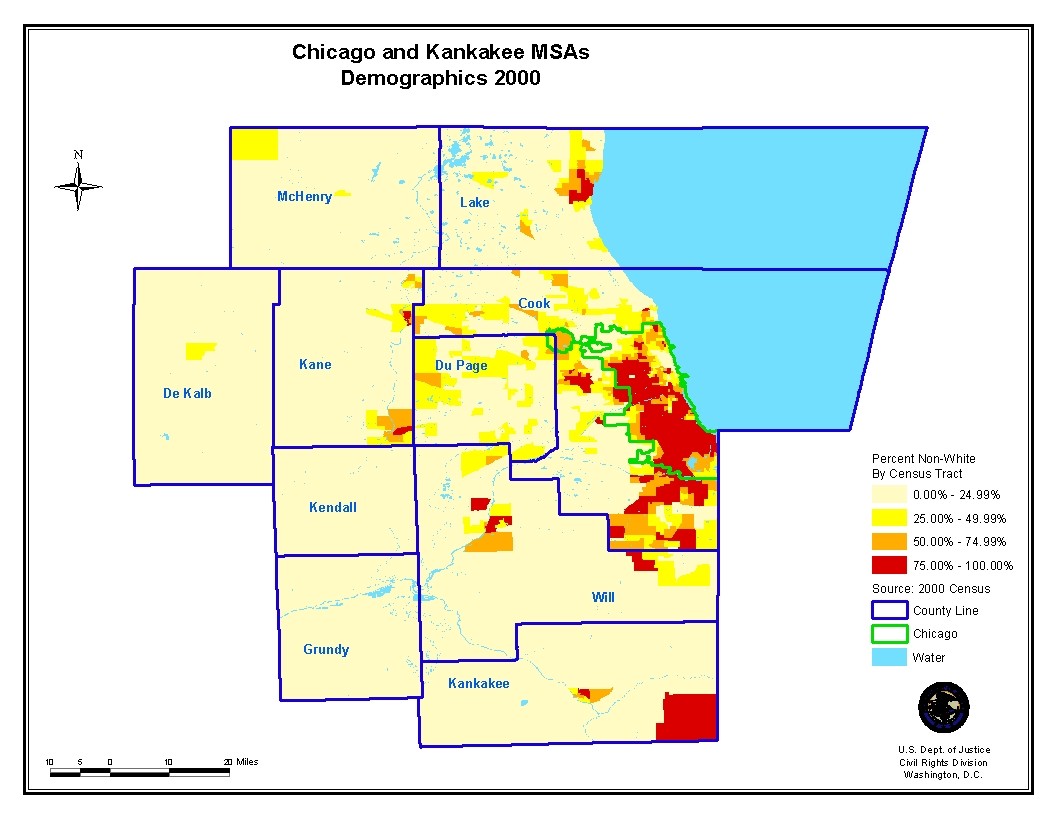

10. Residential housing data for the Chicago MSA show significant patterns of racial and ethnic segregation. According to 2000 Census data, the Chicago MSA is the third-most segregated metropolitan area in the nation for both African Americans and Hispanics of the metropolitan areas with populations of either group above 500,000. According to the 2000 Census, ninety percent (90%) of the Chicago MSA's African American residents and 76% of its Hispanic residents live in Cook County, while 68% of the MSA's African American residents and 53% of its Hispanic residents reside in the City of Chicago. 709 of the 800 majority minority census tracts in the Chicago MSA are majority African American, Hispanic, or combined African American/Hispanic. Eight census tracts are majority Asian and the other 83 minority tracts are a combination of various racial and ethnic minorities. See Map attached as Exhibit 1.

{kind=link}

11. The Kankakee Metropolitan Statistical Area (hereinafter "Kankakee MSA"), as defined by the United States Census, encompasses Kankakee County. The Kankakee MSA, located approximately sixty miles south of Chicago, has 26 census tracts, of which four are majority African American and include over 60% of the MSA's African American population. See Map attached as Exhibit 1.

12. In operating and extending the scope of its business, First American has acted to meet the residential, consumer, and business credit needs of predominantly white residential census tracts (census tracts with a population greater than 50% non-Hispanic white) throughout the Chicago and Kankakee MSAs (here-inafter "the Chicago region"), and has avoided serving the lending and credit needs of majority minority tracts.

13. By the September 1999 consolidation, First American had expanded its business, including that of extending credit for residential real estate-related transactions, home equity, small business, and motor vehicle and other consumer loans, to substantial portions of the Chicago region. In addition to enlarging the geographic scope of the area within which it extends such credit, a major component of the Bank's expansion included the construction or acquisition of additional branch offices, which are designed both to better serve existing customers and to attract new customers to First American's services and products.

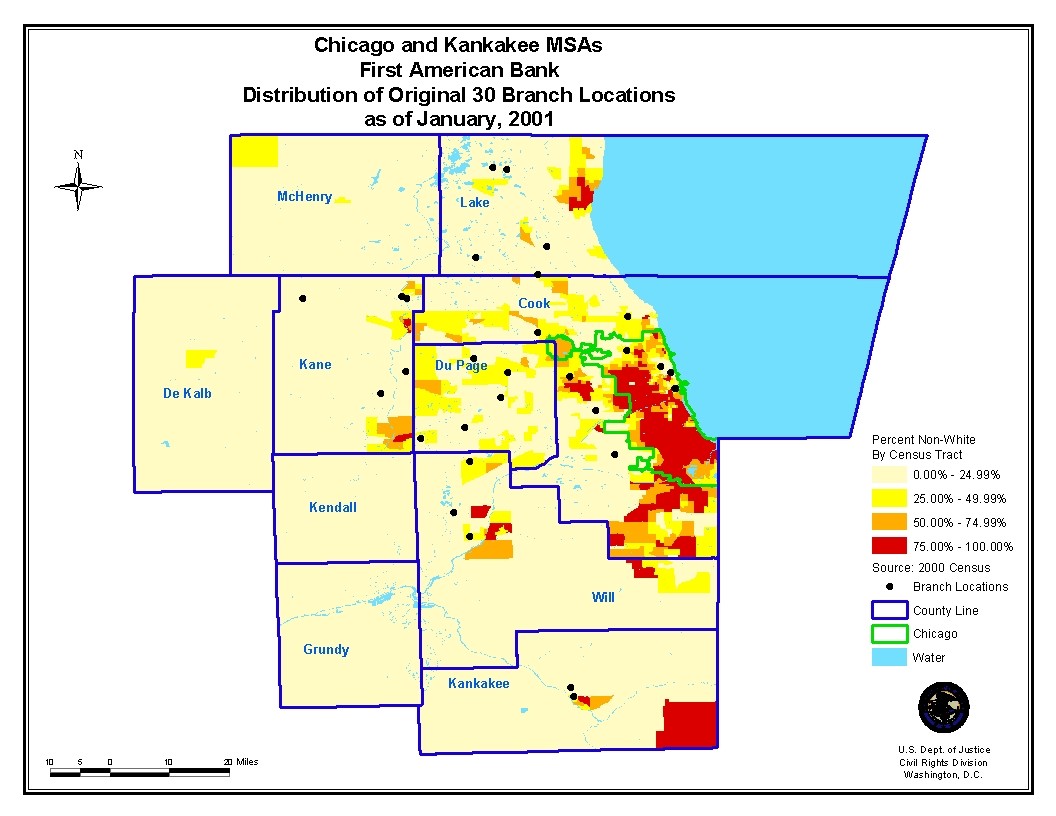

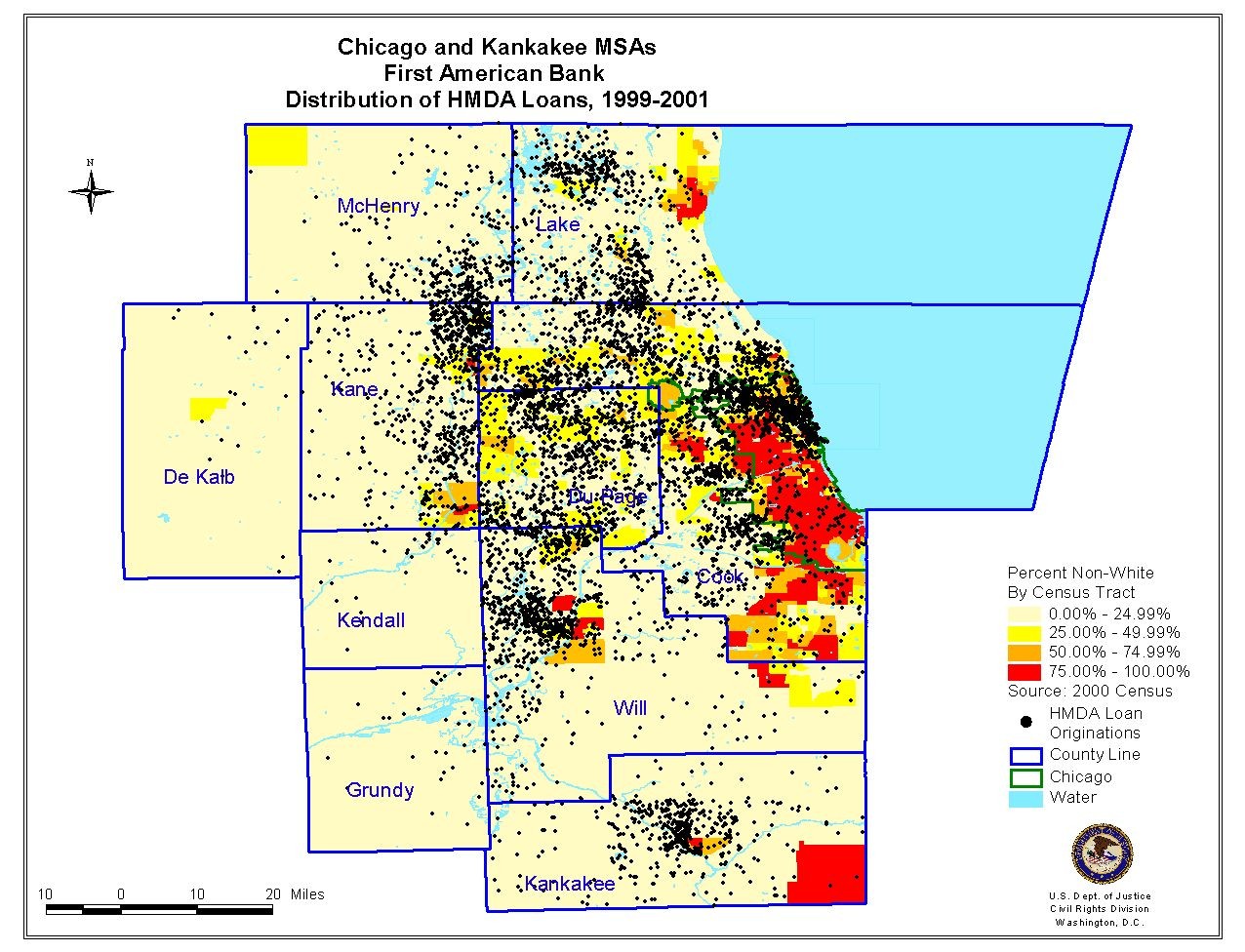

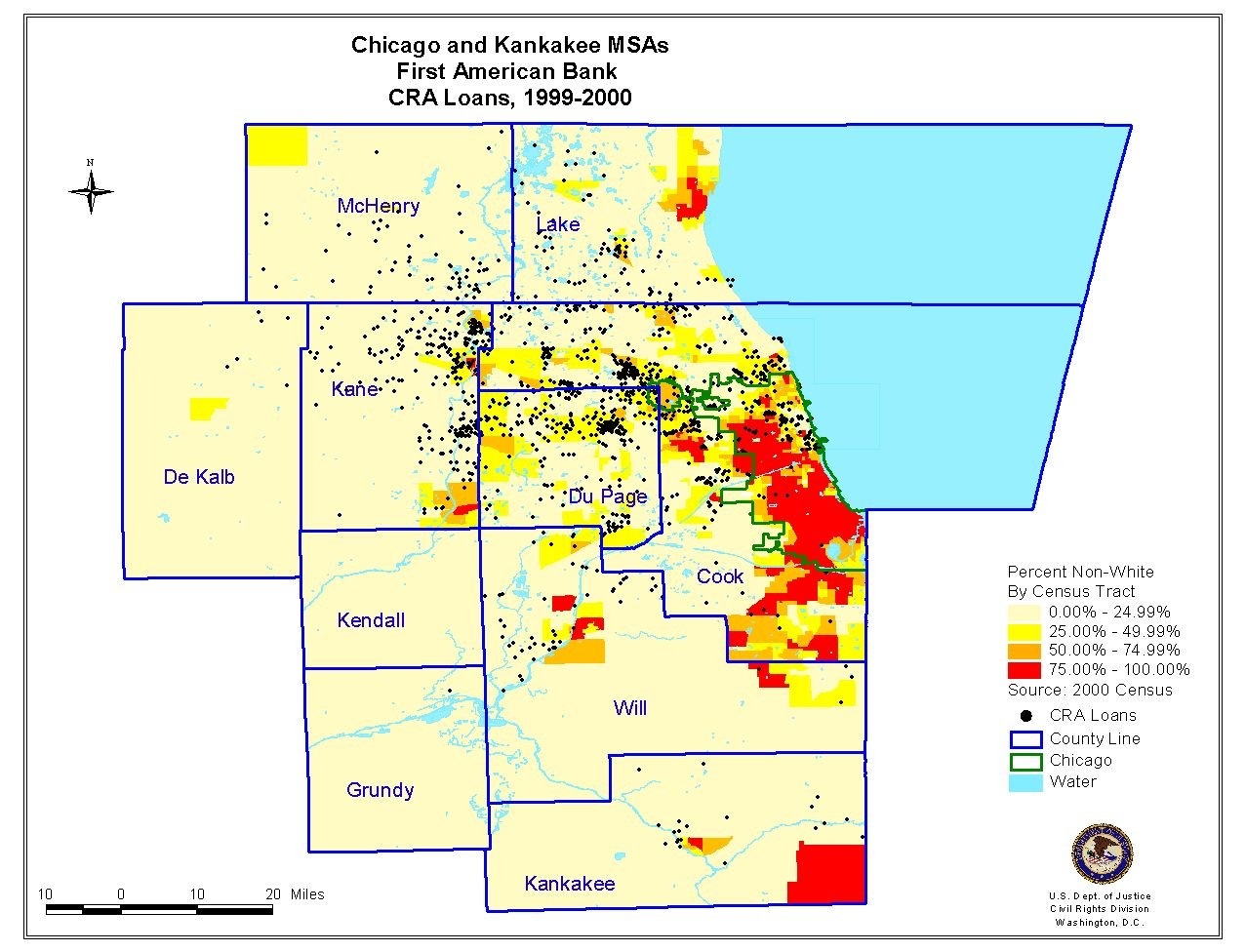

14. First American has engaged in a race and national origin-based pattern of locating or acquiring branch offices. It has located or acquired branch offices to serve the residential, consumer, and small business lending and credit needs of majority white census tracts but not those of majority minority tracts. In January, 2001, when the Federal Reserve Board commenced its compliance examination, First American had 30 branch offices in the Chicago region. None of those 30 branches are located in a majority minority census tract. According to the 2000 Census, the 30 branches are located in majority white census tracts in which minority populations range from 0.6% to 26.7%. See Map attached as Exhibit 2.

{kind=link}

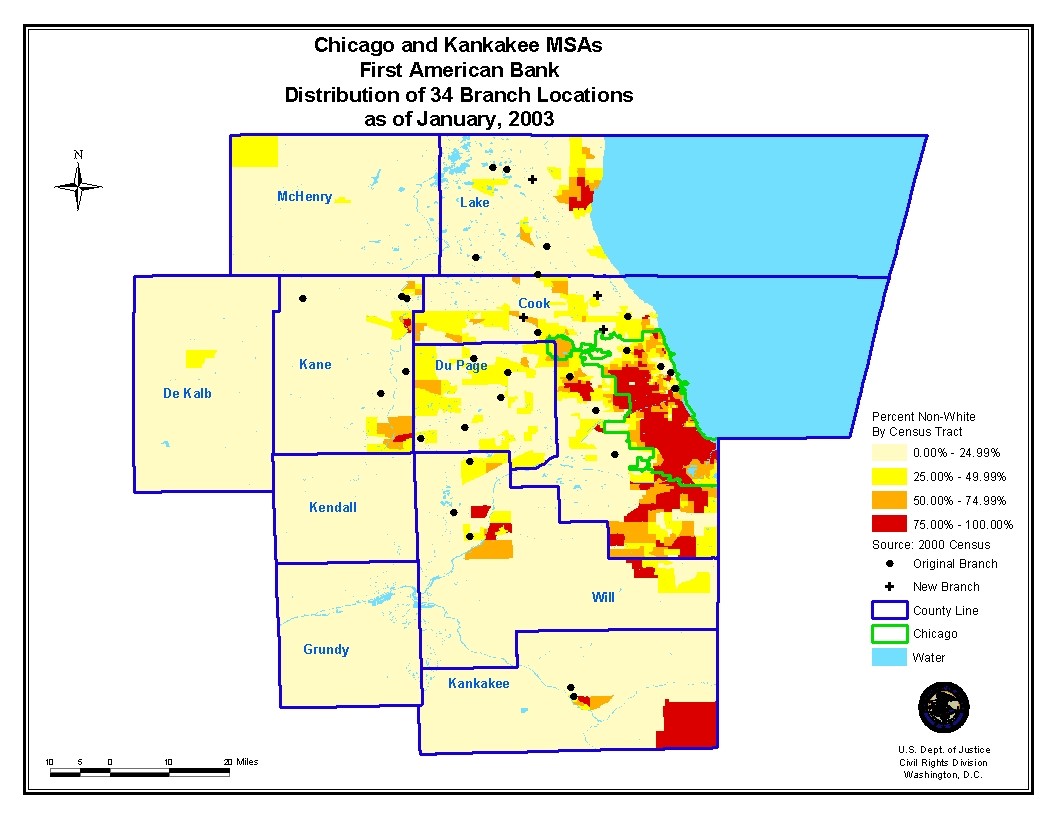

15. Over the next two years, the Bank continued its race and national origin-based pattern of adding or acquiring new branch offices to serve only white communities. By January 2003, First American had 34 branches, with three new ones in Cook County and one in Lake County. All four of these new bank branches are located in majority white areas. See Map attached as Exhibit 3.

{kind=link}

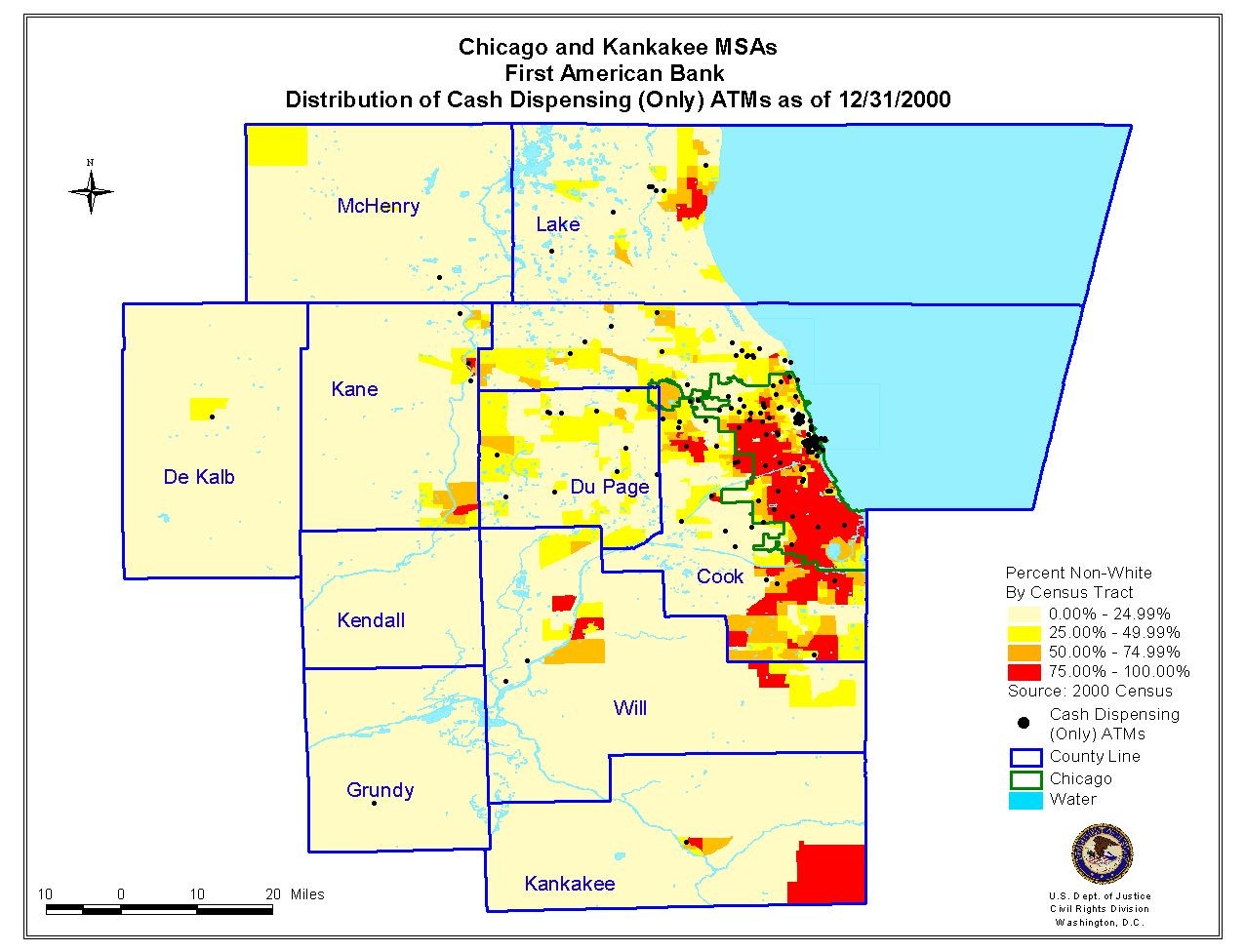

16. Race and national origin considerations also underlie the distribution of First American's Automated Teller Machines ("ATMs"). As of January 2001, the Bank had 78 full-service ATMs (deposit taking and cash-dispensing) in the Chicago region. None of the Banks's full-service ATMs was located in a majority minority census tract. However, the Bank had chosen to locate 18 (approximately 10%) of its cash-dispensing-only ATMs (also called "CDMs") in minority census tracts. See Maps of ATMs and CDMs attached as Exhibits 4 and 5, respectively.

{kind=link}

{kind=link}

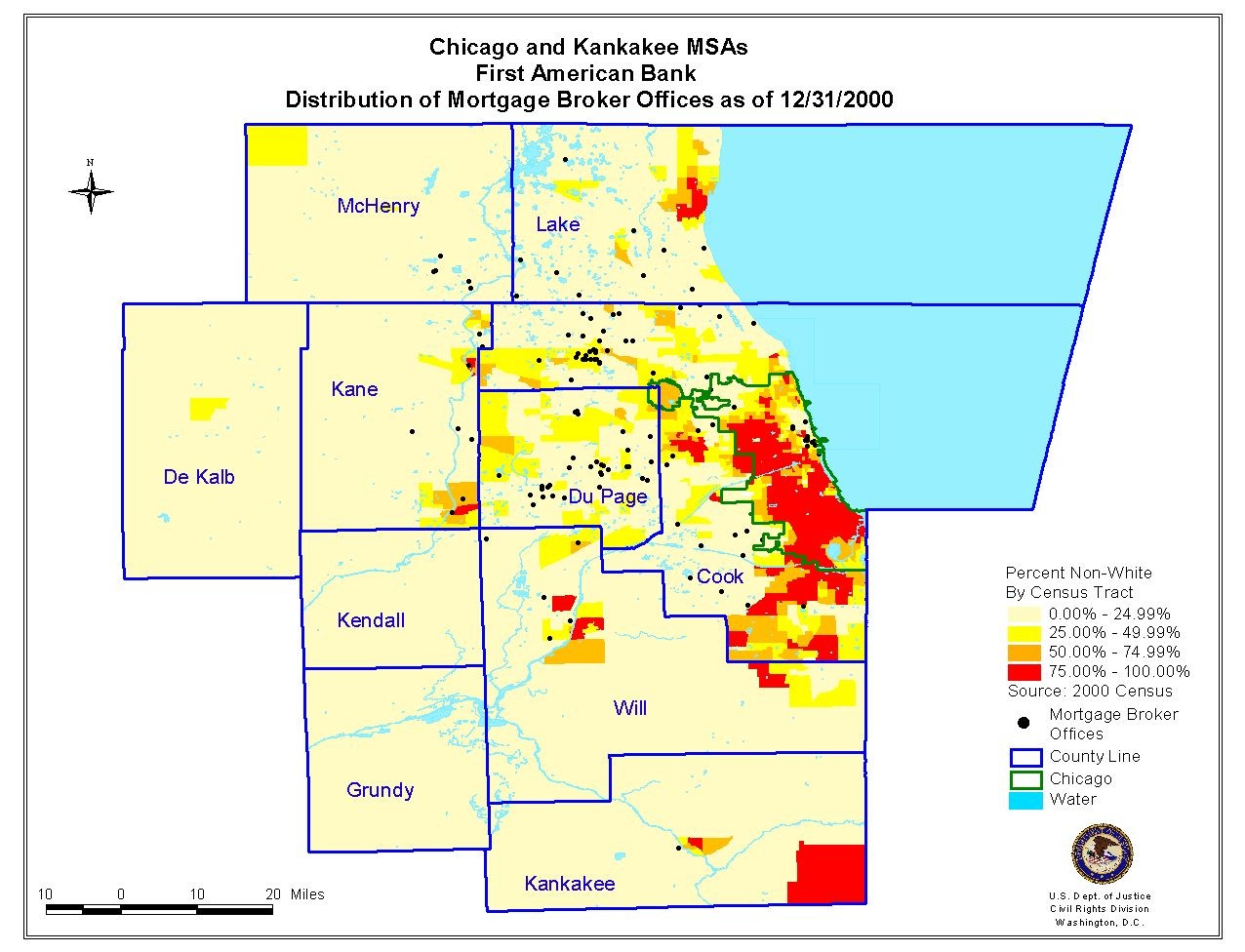

17. First American has actively solicited credit transactions through a variety of discriminatory means, including, but not limited to, the use of mortgage brokers primarily serving white communities in the Chicago region. As of January 2001, the Bank had a mortgage broker network of 122 offices, all but one in the Chicago MSA. Of that total, 97.5% (119) were located in majority white census tracts and only 2.5% (3) were located in minority tracts, each of which have small populations. See Map attached as Exhibit 6.

{kind=link}

18. The unlawful consideration of race and national origin in the business practices and customer solicitation efforts of First American is also evident from its advertising and marketing practices, including, but not limited to, its radio and newspaper advertising focus. The Bank has directed its radio advertising to stations that target "general audiences", although many minority format stations exist in the Chicago MSA market. In advertising its products and services through the media, First American never utilized radio stations oriented to minority communities in the Chicago MSA until after the Board's criticism of those advertising practices.

19. The Bank has also consistently directed its print media advertising to daily newspapers of general circulation and neighborhood and suburban weekly newspapers serving largely non-minority city neighborhoods and suburbs in the Chicago MSA. Until at least December 2002, the Bank had never advertised in minority-focused publications, many of which have larger circulations than some suburban newspapers the Bank has used.

20. The unlawful consideration of race and national origin in the business and customer solicitation efforts of the Bank is also evident from the community service, or assessment area, boundaries that First American has established under the Community Reinvestment Act. In establishing and modifying its assessment area over time, First American long excluded nearly all predominantly minority neighborhoods in the Chicago MSA. Pursuant to statutory direction, the Federal Reserve Board promulgated regulations to implement the CRA, 12 C.F.R. §228 ("Reg BB"). Under Reg BB, as amended in 1997, a large bank's assessment area must generally consist of one or more metropolitan areas or contiguous political subdivisions, §228.41(b), unless that area would be extremely large, of unusual configuration, or divided by significant geographic barriers, §228.41(d). Reg BB further provides that, if a large bank's assessment area does not include entire political jurisdictions, its assessment area may not reflect illegal discrimination. §228.41(e). First American's assessment area historically has not included entire political subdivisions, such as the City of Chicago or all of Cook and Kankakee Counties. The inclusion of these entire jurisdictions would not create an assessment area which would be extremely large, of unusual configuration, or divided by significant geographic barriers, the only exceptions specifically permitted by Reg BB.

21. Instead of defining its assessment area in accordance with Reg BB, First American has circumscribed its lending area in the Chicago region to exclude most majority minority neighborhoods. For example, in 1998, the Bank delineated six highly irregularly-shaped assessment areas, and, in late 1999, it reconfigured them to consist of two distinct areas of the Chicago and Kankakee MSAs. The Bank's Chicago MSA assessment area delineation excluded most minority communities in the Chicago MSA, despite a large number of them being adjacent to the non-minority tracts included in the assessment area. The Bank's 1999 Chicago MSA assessment area included portions of six counties - Cook, DuPage, Kane, McHenry, Lake, and DeKalb - and its Kankakee assessment area included only a portion of that county. The 1999 Chicago MSA assessment area included 792 census tracts, of which only 51, 6.4%, had a population that was majority minority. In the Chicago MSA, over 34% of the census tracts were majority minority according to the 1990 census and over 42% were majority minority according to the 2000 census. The Bank has not provided any nondiscriminatory rationale for its irregular, atypical assessment areas, not even the most rudimentary objective methodology allegedly used to define them. See Map attached as Exhibit 7.

22. Only in March 2001, after the Federal Reserve Board's compliance examiners expressed concern to Bank management about the assessment areas' exclusion of virtually all minority census tracts, did First American change its assessment area delineation to include all of the Chicago and Kankakee MSAs.

23. First American Bank officials have also made statements to examiners from the Federal Reserve Bank of Chicago with respect to the Bank's lending practices which are based on racial and ethnic stereotypes. Among those statements were ones which: (a) indicated that the Bank did not provide the full range of its services and lending products to minority borrowers because they were allegedly not interested in the full range of services the Bank offered to white customers; (b) indicated that the Bank did not provide the full range of its services and lending products to minority borrowers because they were allegedly qualified only for government-subsidized lending programs; and, (c) equated making loans in low income or minority neighborhoods with making bad loans.

24. Analyses of First American's residential real estate-related loan applications for 1999-2001 show that First American has served the credit needs of predominantly white census tracts of the Chicago region to a significantly greater extent than it has served the credit needs of predominantly minority neighborhoods.

25. From 1999-2001, First American generated 10,365 residential real estate-related loan applications in the Chicago region, but only 705, or 6.8%, were secured by residential property located in majority minority census tracts. See Map attached as Exhibit 8.

{kind=link}

26. In contrast, the percentage of such applications in the Chicago region which were secured by residential property located in majority minority census tracts for the aggregate of all Chicago and Kankakee MSA lending institutions was 20.8%, more than three times higher than First American's.

27. In connection with the Board's 2001 fair lending examination, First American identified a group of twelve "peer" institutions to which it recommended its lending performance be compared. Of the total residential real estate-related loan applications submitted to this "peer group" in each year from 1999-2001, First American's percentage from majority minority census tracts ranged from 6.2% to 7.3% annually. In contrast, the percentage of such applications for the aggregate of this self-selected "peer group" ranged from 16% to 26% each year.

28. The geographic distribution of the dollar amounts of residential real estate-related loans funded by First American also demonstrates the consistently stark racial and national origin division in its residential lending activities. Between 1999 and 2001, First American funded nearly $287,892,000 in single-family residential real-estate related loans in the Chicago region. Only 4.5%, about $13,087,000, went to majority minority census tracts.

29. The business policies and practices of First American described in ¶¶12-24 above have achieved the Bank's objective of serving white communities and not minority communities, as further demonstrated by the Bank's overall residential, consumer, and small business lending over time.

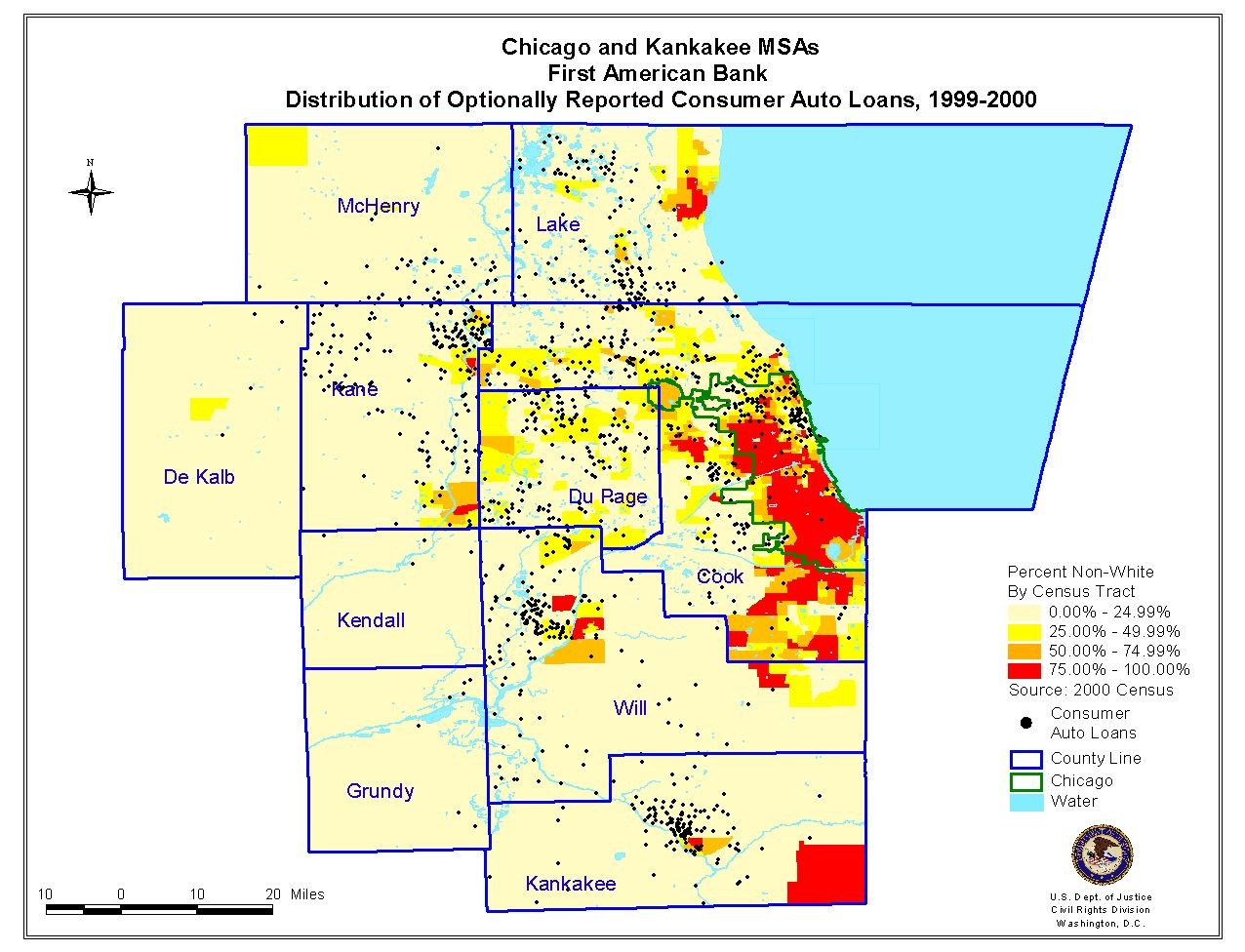

30. In 1999, the Bank originated a total of 7,054 loans in the following categories - residential real estate-related, home equity, motor vehicle, other secured consumer, other unsecured consumer, small business, and other small business. Of that loan total, only 274, or 3.9%, were made in majority minority census tracts. In 2000, the Bank originated a total of 7,069 loans in those seven categories, of which only 308, or 4.4%, were made in majority minority census tracts. Of the combined total of 14,123 such loans the Bank originated in 1999 and 2000, only 4.1% were made in majority minority census tracts in a region where 34% of the census tracts were majority minority in 1990. 31. For 1999-2000, the Bank originated 1,226 motor vehicle loans of which 97.6% (1196) were made in majority white census tracts and only 2.4% (30) in majority minority tracts. The strikingly low percentage of such loans in minority census tracts, despite the widespread ownership of automobiles by consumers in neighborhoods of varying racial or ethnic characteristics, evidences the Bank's intentional exclusion of minority communities from its lending operations. See Map attached as Exhibit 9.

{kind=link}

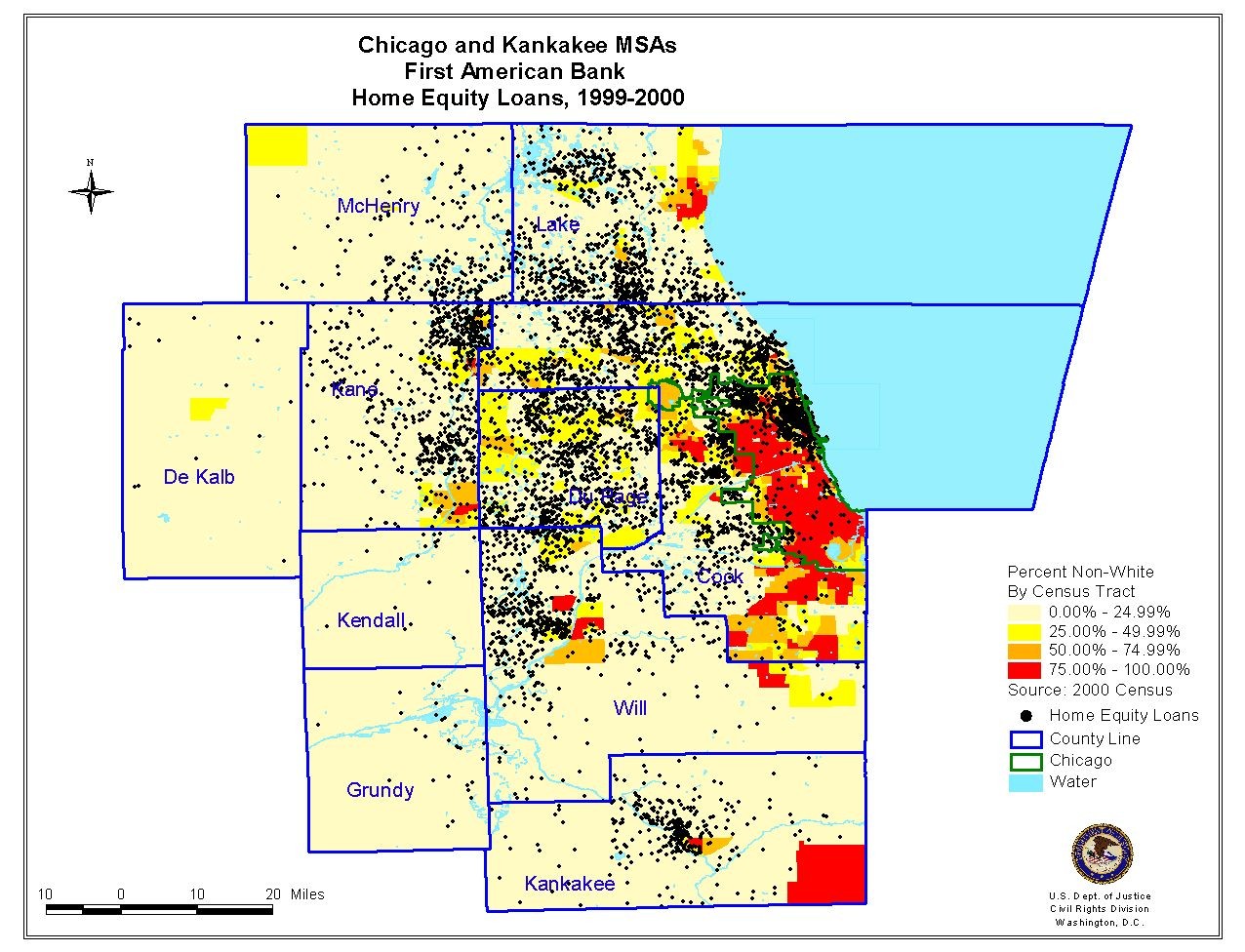

32. Further demonstrating First American's redlining practices is the demographic distribution of its largest volume credit product - home equity loans. In 1999-2000, the Bank originated 6,365 home equity loans, of which 96.2% (6,123) were in majority white tracts and only 3.8% (242) were in minority tracts despite the fact that 33% of the Chicago region's housing stock is located in minority census tracts. See Map attached as Exhibit 10.

{kind=link}

33. The Bank's CRA small business loan originations for 1999-2000 show the same discriminatory pattern and practice. Of the 1,330 CRA small business loans the Bank originated in the Chicago/Kankakee MSAs, 1,268 (95.3%) were made in majority white census tracts, and only 62 (4.7%) in minority tracts in a region which has among the highest number of minority-owned businesses in the nation, over 95,000. See Map attached as Exhibit 11.

{kind=link}

34. The totality of First American's policies and practices described herein constitute the redlining of majority minority neighborhoods of the Chicago and Kankakee MSAs as off-limits for the defendant's lending business. The Bank's policies and practices are intended to deny and discourage, and have the effect of denying or discouraging, an equal opportunity to residents of minority neighborhoods, on account of the racial and/or national origin composition of those neighborhoods, to obtain residential real estate-related credit, consumer credit, and business credit. These policies and practices are not justified by business necessity or legitimate business considerations.

35. The defendant's actions as alleged herein constitute:

- Discrimination on the basis of race, color, and national origin in making available residential real estate-related transactions, in violation of the Fair Housing Act, 42 U.S.C. §3605(a);

- The making unavailable or denial of dwellings to persons, because of race, color, and national origin, in violation of the Fair Housing Act, 42 U.S.C. §3604(a);

- Discrimination on the basis of race, color, and national origin in the terms, conditions, or privileges of the provision of services or facilities in connection with the sale or rental of dwellings, in violation of the Fair Housing Act, 42 U.S.C. §3604(b); and

- Discrimination against applicants with respect to credit transactions, on the basis of race, color, and national origin, in violation of the Equal Credit Opportunity Act, 15 U.S.C. §1691(a)(1).

36. The defendant's policies and practices as alleged herein constitute:

- A pattern or practice of resistance to the full enjoyment of rights secured by the Fair Housing Act, 42 U.S.C. §§3601 et seq., and the Equal Credit Opportunity Act, 15 U.S.C. §1691e(h); and

- A denial of rights granted by the Fair Housing Act to a group of persons that raises an issue of general public importance.

37. Persons who have been victims of the defendant's discriminatory policies and practices are aggrieved persons as defined in 42 U.S.C. §3602(i) and as described in the Equal Credit Opportunity Act, 15 U.S.C. §1691(e)(i), and have suffered damages as a result of the defendant's conduct in violation of both the Fair Housing and the Equal Credit Opportunity Acts, as described herein.

38. The discriminatory policies and practices of the defendant were, and are, intentional and willful, and have been implemented with reckless disregard for the rights of residents of minority neighborhoods.

WHEREFORE, the United States prays that the Court enter an ORDER that:

(1) Declares that the policies and practices of the defendant constitute a violation of Title VIII of the Civil Rights Act of 1968, as amended by the Fair Housing Amendments Act of 1988, 42 U.S.C. §§3601-3619, and the Equal Credit Opportunity Act, 15 U.S.C. §§1691-1691f;

(2) Enjoins the defendant, its agents, employees, and successors, and all other persons in active concert or participation with the defendant, from:

(A) Discriminating on account of race, color, or national origin in any aspect of their business practices;

(B) Failing or refusing to take such affirmative steps as may be necessary to restore, as nearly as practicable, the victims of the defendant's unlawful practices to the position they were in but for the discriminatory conduct;

(C) Failing or refusing to take such affirmative steps as may be necessary to prevent the recurrence of any discriminatory conduct in the future and to eliminate, to the extent practicable, the effects of the defendant's unlawful practices, including redefining its CRA assessment area in accordance with the CRA and its implementing regulations, without regard to race, color, or national origin, and providing policies and procedures to ensure all segments of the defined area are served without regard to prohibited characteristics;

(3) Awards monetary damages to all the victims of the defendant's discriminatory policies and practices for the injuries caused by the defendant, pursuant to 42 U.S.C. §3614(d)(1)(B) and 15 U.S.C. §1691e(h);

(4) Awards punitive damages to all the victims of the defendant's discriminatory policies and practices, pursuant to 42 U.S.C. §3614(d)(1)(B) and 15 U.S.C. §1691e(h); and

(5) Assesses a civil penalty against the defendant in an amount authorized by 42 U.S.C. §3614(d)(1)(C), in order to vindicate the public interest.

The United States further prays for such additional relief as the interests of justice may require.

| John Ashcroft |

| Patrick J. Fitzgerald United States Attorney _____________________________ Joan Laser Assistant United States Attorney 219 South Dearborn Street Chicago, IL 60604 (312) 353-1857 | ______________________________ R. Alexander Acosta Assistant Attorney General Civil Rights Division ______________________________ Steven H. Rosenbaum Chief, Housing and Civil Enforcement Section ______________________________ Donna M. Murphy Deputy Chief ______________________________ Valerie R. O'Brian Burtis M. Dougherty Attorneys U.S. Department of Justice Civil Rights Division Housing and Civil Enforcement Section 950 Pennsylvania Avenue, N.W. Washington, D.C. 20530 (202) 514-4751 |

Document Filed: July 13, 2004 > >